The Mortgage Loan Officer (MLO) exam is designed to assess the knowledge and skills of prospective state-certified loan officers.

Click “Start Test” above to take a free Loan Officer practice test, and check out our premium-quality Loan Officer test prep resources by clicking the links below!

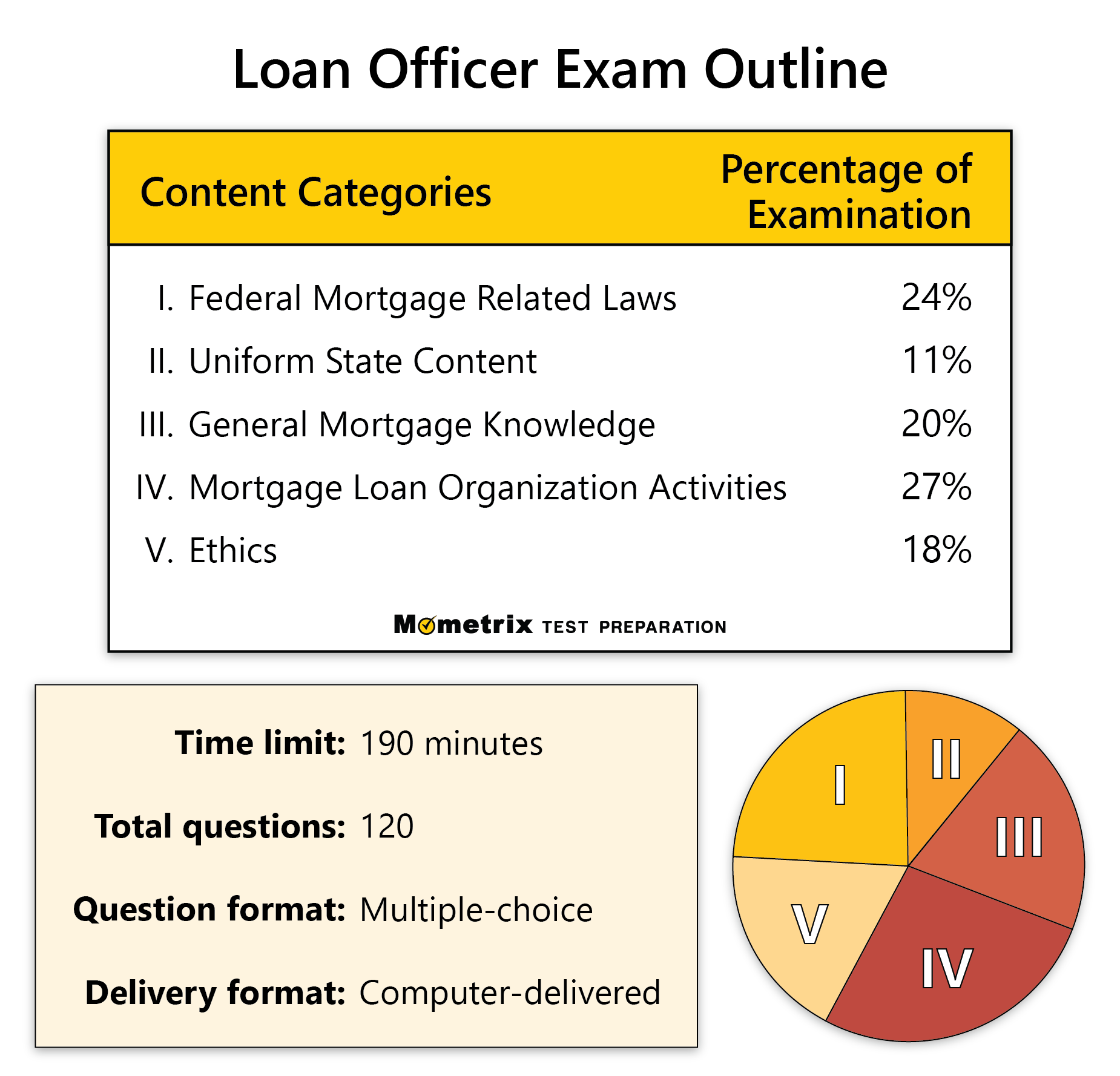

Loan Officer Exam Outline

The MLO exam contains 120 multiple-choice questions, five of which are unscored, and you will be given a time limit of 190 minutes. The five unscored questions are used by the administrators to evaluate questions for future versions of the exam.

The exam is split into five content areas.

I. Federal Mortgage Related Laws (24%)

The questions in this area assess your knowledge of the following:

- Real Estate Settlement Procedures Act (RESPA), 12 CFR Part 1024 (Regulation X)

- Equal Credit Opportunity Act (ECOA), 12 CFR Part 1002 (Regulation B)

- Truth in Lending Act (TILA), 12 CFR Part 1026 (Regulation Z)

- TILA-RESPA Integrated Disclosure Rule (TRID)

- Other federal laws and guidelines

- Regulatory authority

II. Uniform State Content (11%)

The questions in this area assess your knowledge of the following:

- SAFE Act

- State mortgage regulatory agencies

- License law and regulation

- Compliance

III. General Mortgage Knowledge (20%)

The questions in this area assess your knowledge of the following:

- Qualified and non-qualified mortgage programs

- Mortgage loan products

- Terms used in the mortgage industry

IV. Mortgage Loan Organization Activities (27%)

The questions in this area assess your knowledge of the following:

- Loan inquiry and application process requirements

- Qualification: processing and underwriting

- Closing

- Financial calculations

V. Ethics (18%)

The questions in this area assess your knowledge of the following:

- Ethical issues

- Ethical behavior related to loan organization activities

Check Out Mometrix's Loan Officer Study Guide

Get practice questions, video tutorials, and detailed study lessons

Get Your Study Guide

Loan Officer Exam Registration

Registration begins by establishing an online account with the National Mortgage Licensing System (NMLS). Once you have an account, you must create and pay for a testing window, which costs $110. You must then sign a confidentiality agreement, after which you will be able to schedule your examination appointment with Prometric.

Test Day

In-person Testing

On exam day, you should arrive at the testing center about 30 minutes before your scheduled appointment. Once you arrive, you will need to present one valid, government-issued ID with a signature. Your first and last name on the ID must match the first and last name you registered under.

All personal items, such as your cell phone, wallet, and keys, must be placed in a secure locker outside the testing room. Eyeglasses may be inspected before you enter the testing room.

Once you have completed the pre-test procedures, you are directed to your testing station, and your test begins.

Remote Testing

You can sign into the test delivery platform 30 minutes before your appointment. You will need the confirmation number from the email you received after registering, and you must present one valid, government-issued ID with a signature to the proctor. Your first and last name on the ID must match the first and last name you registered under.

Before beginning the exam, the proctor will direct you to move the webcam around your testing space, and your clothing will be inspected visually. You may be asked to pull your hair back, roll your sleeves up and turn your pockets inside out.

Once the proctor is satisfied with your space and workstation and you have completed the pre-test activities, your exam begins.

How the Loan Officer Exam is Scored

To be granted a license to work as a loan officer, the NMLS requires you to answer at least 75% of the questions correctly.

The exam is scored using the Linear On-the-Fly Testing (LOFT) method. The reason for this method is that all of the questions on the exam are not equal in difficulty. If you receive an exam that is created using questions that are more difficult than questions used on another version of the exam, the scoring takes this into account. This method of scoring allows each candidate to have the same opportunities to make a passing grade, even if one takes a test that is considered to be more difficult.

Retaking the Loan Officer Exam

It is possible to retake the MLO exam if you do not pass. You are allowed to take the exam several times, but there is a waiting period from the time you take the exam until you will be eligible to take the exam again.

If you fail to pass the exam after three attempts, you will have to wait a mandatory 180 days before you can try again. The test taken after the mandatory 180-day waiting period will count as an initial exam and start the process of 30-day waiting intervals should you fail to pass.

If you pass the exam, you cannot take it again in hopes of improving your score.

Check Out Mometrix's Loan Officer Flashcards

Get complex subjects broken down into easily understandable concepts

Get Your Flashcards

How to Pass the Loan Officer Exam

How to Study Effectively

Your success on test day depends not only on how many hours you put into preparing but also on whether you prepared the right way. It’s good to check along the way to see whether your studying is paying off. One of the most effective ways to do this is by taking Loan Officer practice tests to evaluate your progress. Practice tests are useful because they show exactly where you need to improve. Every time you take a free Loan Officer exam practice test, pay special attention to these three groups of questions:

- The questions you got wrong

- The ones you had to guess on, even if you guessed right

- The ones you found difficult or slow to work through

This will show you exactly what your weak areas are and where you need to devote more study time. Ask yourself why each of these questions gave you trouble. Was it because you didn’t understand the material? Was it because you didn’t remember the vocabulary? Do you need more repetitions on this type of question to build speed and confidence? Dig into those questions and figure out how you can strengthen your weak areas as you go back to review the material.

Answer Explanations

Additionally, many Loan Officer practice tests have a section explaining the answer choices. It can be tempting to read the explanation and think that you now have a good understanding of the concept. However, an explanation likely only covers part of the question’s broader context. Even if the explanation makes sense, go back and investigate every concept related to the question until you’re positive you have a thorough understanding.

Comprehend Each Topic

As you go along, keep in mind that the Loan Officer practice test is just that: practice. Memorizing these questions and answers will not be very helpful on the actual test because it is unlikely to have any of the same exact questions. If you only know the right answers to the sample questions, you won’t be prepared for the real thing. Study the concepts until you understand them fully, and then you’ll be able to answer any question that shows up on the test.

Strategy for Practice

When you’re ready to start taking practice tests, follow this strategy:

- Remove Limitations. Take the first test with no time constraints and with your notes and MLO study guide handy. Take your time and focus on applying the strategies you’ve learned.

- Time Yourself. Take the second practice test “open book” as well, but set a timer and practice pacing yourself to finish in time.

- Simulate Test Day. Take any other practice tests as if it were test day. Set a timer and put away your study materials. Sit at a table or desk in a quiet room, imagine yourself at the testing center, and answer questions as quickly and accurately as possible.

- Keep Practicing. Keep taking practice tests on a regular basis until you run out of practice tests or it’s time for the actual test. Your mind will be ready for the schedule and stress of test day, and you’ll be able to focus on recalling the material you’ve learned.

FAQs

Q

How hard is the MLO exam?

A

The exam is considered to be moderately difficult, with a first-time passing rate of 58%.

Q

How many questions are on the MLO exam?

A

There are 120 multiple-choice questions on the exam.

Q

How long is the MLO exam?

A

The time limit for the exam is 109 minutes.

Q

What is the passing score for the MLO exam?

A

To pass the exam, you must answer at least 75% of the questions correctly.

Q

How much does the MLO exam cost?

A

The examination fee is $110.